In the run-up to the most contentious U.S. presidential election in living memory, cryptocurrency investors who either can’t stay away for psychological or ideological reasons, or who have to maintain exposure due to institutional exigencies, should be focused on ensuring that they have access to one crucial thing: liquidity.

With election season uncertainties, the ongoing economic effects of the Corona-19 pandemic, and longer-term worries like U.S.-China trade clashes, the ability to enter and exit positions without being forced to sell into a falling market is critically important. That means favoring the most liquid cryptocurrencies. Until election-year political risk recedes, the two biggest players, Bitcoin and Ethereum, are where traders looking to maximize their flexibility should be riding out the storm.

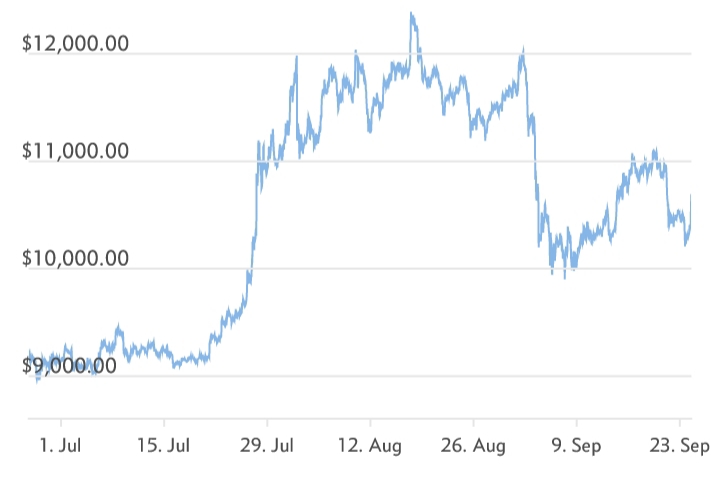

Both cryptos have taken a beating this month, with Bitcoin falling $2,000 in early September before recovering some of its loss. While any sensible investor would be loading up on puts given that volatility, trading volumes show the casino is still popular.

The importance of liquidity in an uncertain market should put Bitcoin, with a $198 billion market cap, at the top of diehard crypto enthusiasts’ lists. Ethereum’s market cap is less than a quarter of the size of Bitcoin’s, but it still dwarfs most of the other cryptocurrencies.

Bitcoin and Ethereum are defensive plays (if such a term has any meaning in the world of cryptos), but also have some upside potential right now. They should benefit from recent regulatory changes that will open the cryptocurrency market to significant inflows of institutional capital. Most of this capital will go into cryptocurrency “household names” with proven track records.

However, the most compelling reason to favor Bitcoin and Ethereum is simply good risk management. The specter of a contested election has become the second-most pressing concern for global investors, after the coronavirus, according to Bank of America Securities monthly fund manager survey. Until those two risks subside, the volatility they could cause across various markets will affect investors’ risk appetites and therefore their demand for cryptocurrencies. Those cryptocurrencies with small market capitalizations could be subject to sharper swings in price.

This is similar to what happened to the high-flying stocks of the dotcom era. Many of the dotcom superstars rose to the heights they achieved, despite having no revenues, let alone earnings, because of their microscopic floats. Small changes in demand therefore had large effects on their prices. This was all good when everyone was buying, but it caused small-float dotcom stocks to fall faster than their larger, more established technology brethren when investor sentiment turned in March of 2000.

Some might argue that the higher volatility of smaller cryptocurrencies might be an advantage in this environment, since they could pop more if investors crowd into the sector during a flight to quality. But cryptocurrencies have exhibited the same behavior as other assets during periods of risk aversion this year. Witness Bitcoin’s 50% first-quarter plunge and subsequent rebound, which put it firmly in the “risk asset” camp, along with stocks and junk bonds. Cash and sovereigns apparently remain the risk-off assets of choice in a crisis.

The other good reason to back the big cryptocurrencies as the lesser evils is the decision in July by the Office of the Comptroller of the Currency to allow banks to provide custody services for cryptocurrency accounts. The legal uncertainty about this type of custody business that existed before the OCC’s announcement kept a lot of investor capital from reaching the cryptocurrency markets.

That’s because asset managers seeking to invest in cryptocurrencies have been hamstrung by client guidelines that typically require all securities to be held in custody, usually by Federally chartered banks. Now, asset managers can take advantage of their clients’ demand for cryptocurrency exposures to expand their investments in what they see as a profitable asset class. Cryptocurrency hedge funds, for example, have reaped double digit gains this year, and traditional asset managers want in on the action.

Much of the initial funds flowing from these asset managers into cryptocurrencies will go to those that can be traded both in cash and derivatives markets. Bitcoin, in particular, will benefit from its listed derivatives on CME because asset managers can tailor their risk profiles using Bitcoin futures and options on futures – something that will appeal to their more conservative institutional investor clientele. These listed derivatives also give investors a window into market sentiment about future prices. (Futures traders currently anticipate Bitcoin to end the year just shy of $11,000.)

Of course, listed derivatives such as these can increase volatility in some cases, in part because they are leveraged and can be bought on margin. Witness how call options on FANGMAN stocks drove those shares up in the second quarter as option sellers covered their positions in the cash markets. When sentiment reversed and those cash positions were partly unwound, the situation exacerbated the tech plunge in early September.

Nonetheless, the availability of these hedging tools, alongside the market bulk that Bitcoin and Ethereum exhibit, make them the best-positioned of all the cryptos to ride out any serious market volatility in the coming months.