Commercial real estate market participants had some reasons for optimism in the third quarter. Banks continued to avoid large realized losses on CRE lending. Lower infection rates in some large cities allowed them to ease lockdown measures, benefitting the retail, office and lodging sectors. But despite these promising signs, and irrespective of the near-term course of the pandemic, Covid-19’s long-term effects on the CRE market are shaping up to be profound.

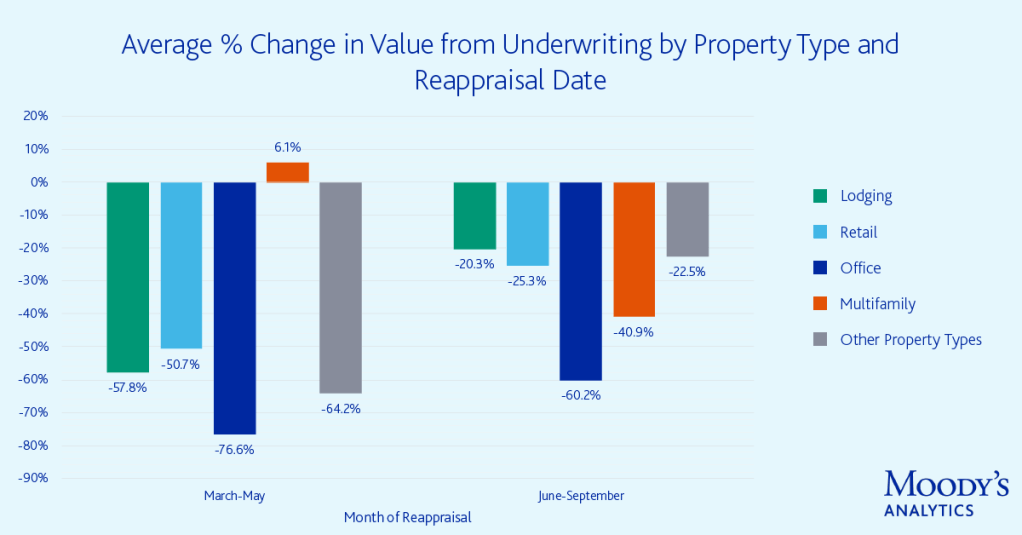

CRE property values continue to fall, although data from Moody’s Analytics shows a decrease in the pace of declines in the third quarter. Even so, office sector properties fared badly, with appraised values of troubled assets falling 77% in the second quarter and 60% in the third.

Although banks do not hold much CMBS, their direct loans are worrying. According to a recent Financial Times analysis of the 10 biggest bank CRE lenders, the size of their problem loan holdings had increased 144% since the beginning of the crisis, to $26 billion. These loans are now equivalent to debt with a rating deep in junk territory – CCC or lower.

Other types of lenders are no better off. The rating agency Fitch says that life insurers will see 50% greater losses on their mortgage loans than they did during the Great Financial Crisis. Fitch also expects U.S. CMBS delinquencies to be near their previous peaks of 8.25-8.75% in the fourth quarter of this year.

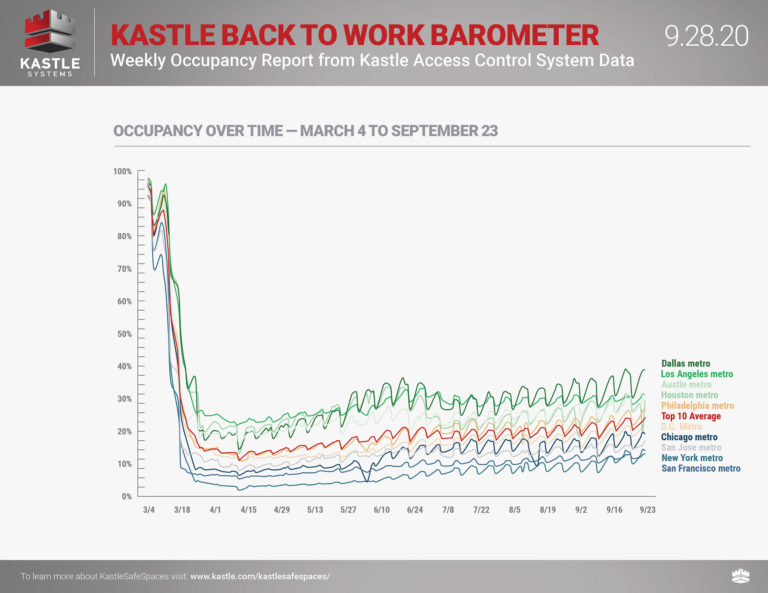

Luckily, there are signs of life returning to some sectors, even office. Kastle Systems, which provides employee monitoring equipment for 41,000 businesses in 47 states, says its ten-city average occupancy index rose to 25.8% at the end of September, up from its April nadir in the mid-teens. Some cities have done significantly better, such as Dallas and Los Angeles. Even New York, the U.S. epicenter of the pandemic, has seen some improvement, although occupancy still languishes at 15.6%, according to Kastle data. San Francisco is at the bottom of the list, with only 14.5% occupancy.

While financing will eventually struggle back, analysts say Corona-19 dislocations will fundamentally change the CRE landscape. In a recent report, Fitch’s structured finance team wrote, “The effects of the pandemic will accelerate secular trends that were already underway prior to the crisis. The pandemic has also introduced new challenges to social and business transactions that will affect retail, office, lodging, industrial and multifamily housing to varying degrees.”

A forecast by Cushman & Wakefield supports this, as it applies to the future of the office sector. According to the firm’s model, the U.S. office market will shed 145 million square feet of space in the next two years. The firm expects office demand to decrease by 30% more than it did during the Great Financial Crisis. Those changes will not be reversed easily. While signs of progress in fighting the pandemic might be encouraging, CRE market participants should temper their optimism with the understanding that this business is undergoing fundamental change, the full extent of which is only now becoming apparent.